2021 was a relatively flat year for gold in developed markets. This was with the exception of a few developing markets like Turkey and Myanmar who bucked this trend where gold rose by 61% and 30% respectively.

This year, all eyes are on interest rates. If they rise, bonds could challenge gold further (because they pay interest, whereas gold does not…yet). But this also contains a conundrum, since rising rates mean falling bond prices (even if bonds do pay some interest along the way).

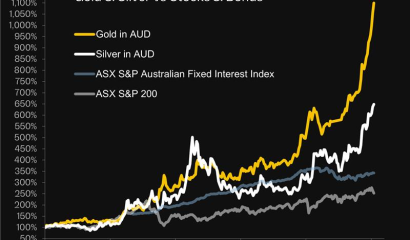

In our 2022 Outlook we talk about possible rate rises, how these could impact the traditional 60/40 stock/bond portfolio, and why it looks like gold may end up being the beneficiary.

Here’s a quick summary of our take, but if you’d like a deeper dive, you can access and view our comprehensive 2022 outlook by heading over to our Outlook 2022 page.

Continue reading

While the numbers have changed and circumstances are constantly fluctuating, the way to look at 2022 will need to be centred on accumulating and diversifying.

- Interest rates are surging and, historically, any rise in interest rates has often been viewed negatively within the context of gold prices. This is a view that we have challenged on previous occasions.

- Oxford Economics have found that a 10-15 per cent gold allocation to the typical 60/40 balanced portfolio reduces the risk of the portfolio while increasing returns.

- There’s an expectation of a return to normalcy but this is going to be a lot harder than we think given the just how debt levels are at the moment.

- 2021’s flat gold prices may signal deflation ahead, which is likely given that the full long-term economic effects of the lockdowns continue to be felt around the world while any stimulus programs related to the lockdowns reach their expiration dates.

- Gold is applying pressure on fiat currencies with banks, in recent months, attempting to defend the $1800 level.

- Staunch defenders of the fiat banking system, from the Fed to the European Central Bank to the IMF and The World Bank, may only have two choices.