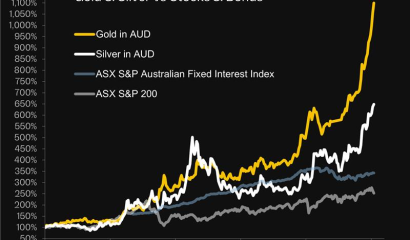

Gold held its value in the first half of 2022 better than almost every other asset class

Total return figures from 1 January through 30 June 2022:

- NASDAQ: -29.3%

- S&P 500: -20.0%

- Emerging Markets Stocks: -17.2%

- U.S. Government Bonds: -21.1%

- Real Estate (XLRE): -20.1%

- ASX 200: -13.4%

- Bitcoin: -59.1%

Gold returns in H1 2022 by country/region:

- U.S.: -1.2%

- Australia: +4.4%

- Europe: +7.03%

- U.K.: + 9.4%

- Japan: +14.4%

Investors just now checking their mid-year statements from their brokers will be considering their options, especially as they see that both sides of a typical 60/40 stock/bond portfolio suffered substantial declines.

Most investors know that stocks can be volatile, so it was the bond market losses that were particularly wrenching. Bank of America stated that bonds “saw the worst declines since 1865”:

As the WSJ notes, bond declines caused by higher interest rates robbed investors of a traditional safe haven. At Rush we have long been signalling that as investors flee bonds (as the 40-year bond bull market ends) they will need to rotate into another capital preservation asset.

Given the size of bond markets globally (+/- $140T), the replacement asset will need to be very widely traded, global, with enormous daily liquidity. Gold is one of the few possible capital preservation options that meets these requirements and could be the recipient of large inflows as a result.

Even if just a portion of the $140T in bonds finds its way into the $12T gold market, over time the upward pressure on gold prices would be significant.

U.S. Dollar strength is a continuing headwind for many markets

Gold is widely traded and quoted in USD, which makes gold and the USD mirror assets. The dollar (shown in the chart below against a basket of 6 major currencies) has hit 20-year highs:

Source: Refinitiv

Gold’s resilience in the face of this dollar rally headwind has been nothing but impressive.

This dollar strength has been driven by companies and investors selling other assets to receive dollars to pay down U.S. dollar denominated debt, in anticipation of an upcoming recession. It has also been exacerbated by rising commodity prices (like oil, which is priced in USD). Both of these factors look set to continue.

Inflation has arrived but action to contain it has not

Interest rates have begun to rise but both the U.S. Government and the Fed are still fuelling the inflationary fire. In March of 2020 the Fed opened the monetary floodgates (again), with their balance sheet soaring from $4.2T to $8.9T in just two years. A new multi-trillion dollar U.S. Government spending package was only narrowly defeated last week and a new version is being prepared.

Here in Australia, they also continue to add petrol to the inflation fire by continuing to print money to pay for ever-higher spending. Yesterday the new government announced another large new entitlement (spending) program, and last month New South Wales announced a 26% increase in government spending over 2021. These are both likely to provide additional upward inflationary pressure.

Echoes of previous stagflationary times

Many analysts are comparing current inflationary conditions to those of the 1970’s. But while the conditions may be largely the same, the available fixes are not.

In the 1970’s Fed Chairman Paul Volcker raised interest rates as high as 20% to slow wages and prices spiralling upward. In just one Fed meeting Volcker raised rates by 500 b.p., a whopping 5% increase in one go.

Similar interest rate hikes would not be possible today, however, as the total government, corporate, and personal debt burdens are simply too large. In particular, the Eurozone looks especially vulnerable to higher interest rates.

The euro currency system, essentially a transfer mechanism to send the savings of northern Europeans to the south, relies on a strong German economy. But short-sighted German energy policy coupled with Ukraine sanctions “blowback” have meant that Germany is now running a trade deficit for the first time in 20 years.

Inflation has already touched 20% in some European countries, and their ability to fight it with higher rates is limited given the economic weakness. And this structurally higher Eurozone inflation could keep inflation elevated around the globe.

If gold reacts to inflation in just a fraction of the way it did in the 1970’s (with gold rising from $35 to more than $800 per ounce), then investors will be thankful they took note of these historical parallels.

Recent gold price weakness in July 2022 could provide the entry point for just such a strategy.