There is no doubt that the trajectory of inflation which almost every nation faces today is instructive for gold investors.

For investors with a lower or transitory inflation outlook, the motivation to protect purchasing power by owning gold would be less urgent. Their view suggests that if inflation were to abate, shares and bonds could rise in value and it would be unnecessary to raise interest rates and depress property and other asset prices.

But what if we see sustained stagflation? Not only is stagflation about high consumer price inflation, it’s also characterised by stagnant or low economic growth. Usually that picture is accompanied by rising unemployment.

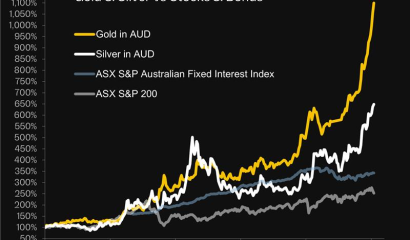

Should stagflation emerge, the circumstances could be a repeat of the 1970s when gold surged from $US 35 to $US 850 as people sought to defend their wealth.

The Sources of Inflation

Investors who hold onto the lower or transitory inflation outlook may need to question the reasoning behind their views.

Inflation is not something that “just happens”. Inflation is a policy choice by governments and by central banks.

Governments choose to create inflation when they borrow and spend. Central banks choose to create inflation as they increase the supply of money in the economy.

For example, the U.S. Government Covid stimulus bills provided 40 per cent more money directly to consumer bank accounts than the income they had lost during the lockdowns. People spent these extra funds on everything from second cars to second homes, driving their prices higher.

On the central bank side, the policy choice is called “inflation targeting”. At the entrance of the Reserve Bank of Australia in Martin Place in Sydney, this policy is clearly spelled out: “The appropriate target for monetary policy in Australia is to achieve an inflation rate of 2–3 per cent, on average, over time”.

In other words, the stated policy of the protector of the value of the nation’s money is to steadily reduce the money’s ability to buy goods and services over time.

And the difference between a targeted outcome of 2-3 per cent inflation versus the current real-world result of 6.1 per cent inflation is one of degree, not of policy. The exact same policy produces both outcomes.

How Did Inflation Targeting Policies Originate?

Inflation targeting policies were implemented after inflation hit 17.7 per cent in 1975. The idea was urgently to get inflation down to 2-3 per cent, not to make sure it stayed at least that high or higher.

The last time we had double digit inflation in Australia, bank term deposits were paying 14.9 per cent interest. That enabled people to maintain their buying power simply by holding bank funds. Today that is not the case.

Supply And Demand Factors Currently Affecting Inflation

Those who believe inflation will be transitory argue that the Covid lockdowns impeded the supply of goods of all kinds, and when these interruptions abate then the supply of goods – and inflation levels – will be restored to previous lower levels.

The Federal Reserve Bank of New York even quantified the percentage of inflation they think has been caused by Covid lockdown supply problems at 40 per cent.

And U.S. Federal Reserve chairman Jay Powell got himself off the hook last week by saying that central banks cannot affect supply side constraints.

A New Supply Shock Factor Emerges

Now a different supply shock must be considered: the supply of energy. This supply has been affected in the short term by sanctions on Russia and over the longer term by increasing reliance on intermittent energy sources.

These energy supply factors are likely to persist long after the Covid lockdown effects taper off. In fact, the growing energy supply crisis is already so severe that the leaders of Europe’s largest metals manufacturers sounded a dire warning at an emergency meeting last week.

These senior members of the European Non-Ferrous Metals Association said that they were deeply concerned that the winter ahead could deliver a decisive blow to many of their operations. They called on European Union and member state leaders to take emergency action to preserve their strategic electricity-intensive industries and prevent permanent job losses. Significantly they noted that half of the EU’s aluminium and zinc capacity had already been forced offline due to the power crisis.

“All metals production needs affordable and available electricity and gas, whether aluminium and zinc today or lithium and cobalt [for renewable technologies] tomorrow. Europe faces a critical situation for the foreseeable future,” the group warned.

https://eurometaux.eu/media/qnhn5k30/non-ferrous-metals-ceo-letter-on-energy-crisis-06-09-2022.pdf

Once again, government policy choices are at the root of the current inflationary spiral. Given the political environment around these policy choices, it’s not difficult to conclude that inflation will be higher, for longer, and that these policies will suppress economic growth in parallel. Both are key ingredients for a classic stagflationary environment.

Inflation Is A Damaging Policy Choice

It’s worth remembering the view of Jeff Deist, the President of economic think tank The Mises Institute. Deist points out that owning a nominally larger quantity of money that can only be exchanged for fewer goods and services is not an increase in wealth, it is a reduction.

The idea that government policies can make us richer, to Deist, is absurd. “More goods and services,” he writes, “produced more and more efficiently, thanks to capital investment—and thereby creating price deflation—make us richer. That’s the only way. Not legislative or monetary edicts”.

https://mises.org/wire/inflation-state-sponsored-terrorism

So it may be prudent to prepare accordingly, by owning inflation resistant assets like gold, before the arrival of even deeper energy shocks as winter arrives in the Northern Hemisphere. Rush Gold makes it easy to do just that.

Download our app now and BUY 100% title to GOLD in minutes