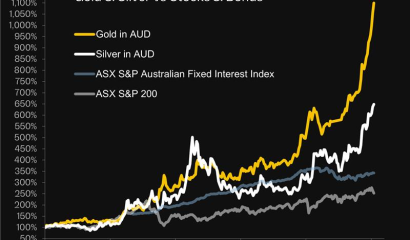

For quite a while we at Rush Gold have identified the potential for gold to displace the capital preservation role of bonds in investor portfolios over time.

Given the relative sizes of the bond market (+/- $100 trillion) and the gold market (+/- $13 trillion), an increase in the flow of money from the former into the latter could place significant long-term upward pressure on gold prices.

This week Bank of America posted data confirming that gold’s competitor in this battle (bonds) are currently in their worst bear market of all time:

Considering that BofA’s historical data goes back 236 years all the way to the founding of the republic, this is quite a jarring statistic.

And the graphic view of the bond decline drives the point home even further:

Isn’t it time for some bond bottom fishing?

A value equity investor would be tempted to look at a decline like the chart above and jump in with both feet. If this was a share market decline, it could be argued that an investor could pick up a viable enterprise for pennies on the dollar.

But bonds don’t work that way. A bond paying 2% interest will continue to trade at a deep discount with current interest rates at 5% or more.

And those intending to hold that 2% bond to maturity would still need to ask themselves: will the bond issuer still be able to pay me my principal at maturity?

This may seem like an academic question if the bond issuer is The United States of America. But the signposts are worrying:

- The U.S. took from its founding until 1975 to accumulate its first $500B in debt. It just did the same in the last 18 days.

- Bond prices are subject to supply and demand. But very large Treasury bond purchasers including the central banks of China, Russia, Japan, Saudi Arabia, Brazil, and others have turned from net buyers to net sellers.

- The Fed itself has ended its bond purchases, as it shifted instead to fighting inflation, ending the era of so-called “quantitative easing”.

- This departure of the Fed from the market has thrust pricing power back onto banks, insurers, and hedge funds. But these market actors are fickle, and trade based on their own narrow P&L metrics, not “national interest” metrics like inflation rates and social and share market stability.

Keep calm and carry on

We are reminded of what the writer Goethe said during a time of great upheavals:

“Be valiant and great forces will come to your aid”

In this case the great force of history’s most reliable wealth protection asset is available to all. In a world awash in debt, mired by conflict, struggling with solvency, and running out of accounting tricks (like QE) that simply mask or postpone insolvency, preserving wealth with bullion deserves a fresh look.