An asset allocation rethink may now be necessary in order to preserve capital

Clues from the marketplace are piling up as the world grapples with a variety of crises.

Coolabah Investments CIO Christopher Joye remarked late last week that “the concern is that central banks have yet to get close to dealing with their inflation woes”.

A few days later Reserve Bank Governor Phillip Lowe surprised markets (and proved Joye’s point) by raising interest rates by a further 0.25%.

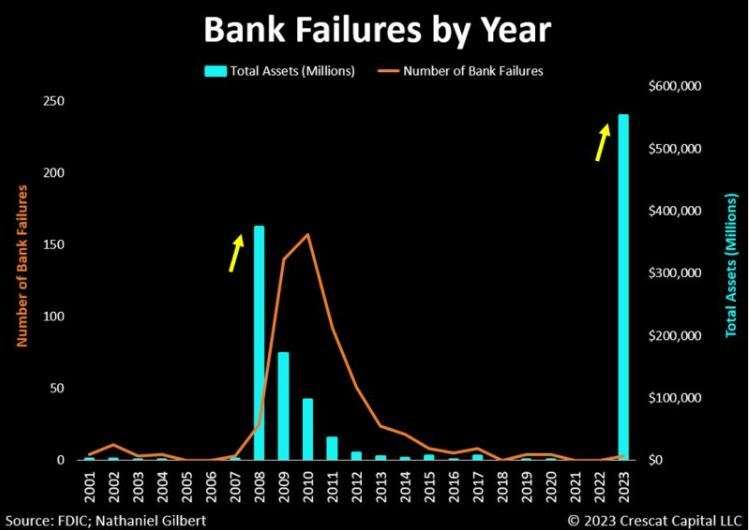

Another clue came with the recent bank collapses in the U.S. (the second, third, and fourth worst in U.S. history), also related to interest rate rises to battle inflation.

In the space of four weeks we saw the collapse of Silvergate Bank (USD $103 B), then Signature Bank (USD $110 B), then Silicon Valley Bank (USD $209 B), and then this week First Republic Bank (USD $213 B).

That accelerating trend is worrisome indeed.

But confusingly, the collapse of First Republic was accompanied by the stock market going up.

What is going on? And what does this mean for those of us trying to preserve our capital through this crisis period?

Currency and banking crises can unfold slowly at first

One of Ernest Hemingway’s characters was asked how he went bankrupt, and he replied: “Two ways. Gradually, then suddenly”.

Many people forget that at the beginning of the GFC, seven months passed between the collapse of Bear Stearns and the collapse of Lehman Brothers. In hindsight it looks like that was the “gradual” part.

On 19 March 2008 Bear Stearns abruptly closed their doors after 134 years.

On 8 June 2008, then Chairman of the U.S. Federal Reserve Ben Bernanke calmed markets by stating that “the risk that the economy has entered a substantial downturn appears to have diminished”.

Then on 15 September 2008 Lehman Brothers collapsed, kicking off the GFC in earnest.

It looks like we may be at the beginning and not the later stages of this banking and currency crisis. Luckily investors may still have some time to position to preserve their capital.

So what should they consider owning?

Put simply, governments print money in response to crises

The Covid crisis saw the Fed doubling their balance sheet in less than 3 years. People should not be surprised that this has led to high inflation around the world as the Covid lockdown bill comes due.

In the case of the banking crisis, the share market rallied on the day of the First Republic bailout because investors realised that even more money printing would be required, which would in turn boost certain asset prices.

Broadly, this is a debt crisis. And to get through a debt crisis the best thing may be to own things that are the opposite of debt.

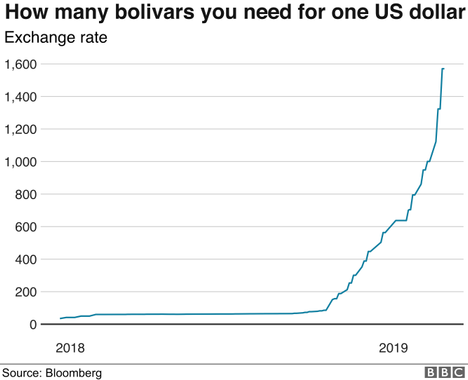

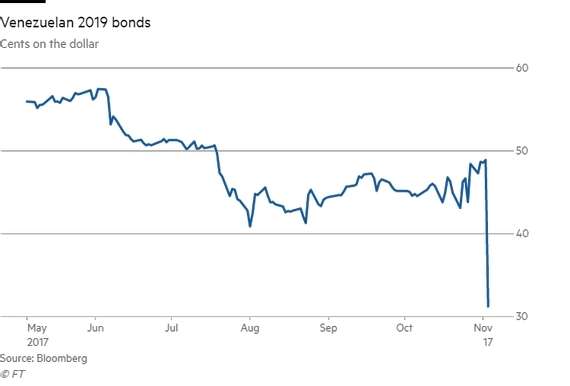

The extreme example of Venezuela shows what to own, and what not to own, in this kind of crisis

The Venezuelan example began when the country’s currency (the bolivar) quickly went from just inflationary (as the AUD and USD are today) to hyperinflationary:

As inflation took off, the chart below shows how Venezuelan bonds were definitely not the asset you wanted to own:

But two asset classes, each of which could be viewed as the opposite of debt, soared in value: shares and gold bullion.

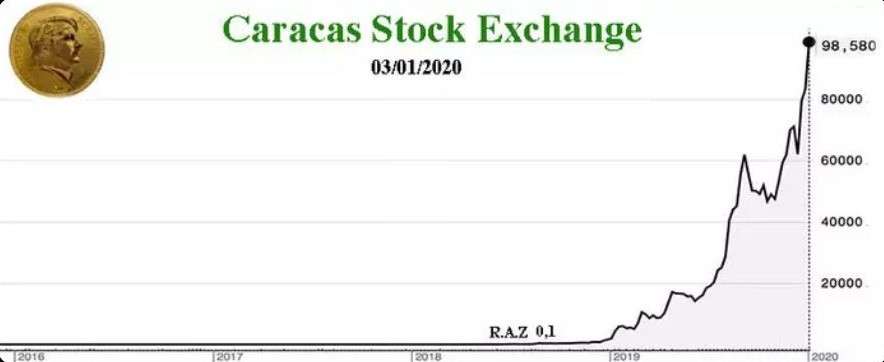

The following chart shows how the Caracas Stock exchange soared when the currency hyperinflated:

Data source: Refinitiv

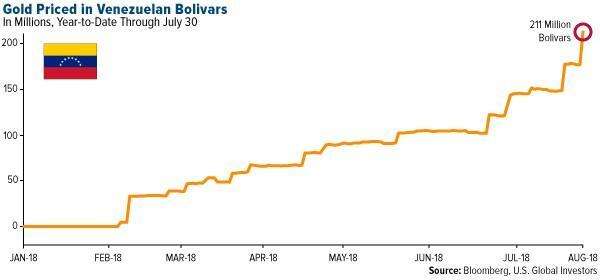

And this chart shows the price of gold soaring to an incredible peak of 211 million bolivars:

Does a new crisis asset allocation model make sense?

Respected macro-economist Luke Gromen has proposed a new asset allocation for investors primarily seeking to survive this crisis period with their wealth intact.

His approach is not to speculate and try to profit from the crisis. Instead, Gromen says that his objective is that when the crisis ends, he still has most or all of his buying power available.

Gromen proposes the following:

- 40% large cap, top quality dividend-paying shares, primarily in energy producing companies

- 20% physical gold bullion (not just bullion ETFs with financial market counterparty risk)

- 20% cash (for opportunistic purposes as desirable hard assets get mispriced during market panic periods)

- 20% other “hard” assets. Gromen’s list includes assets like cash generating farmland, unique selected real estate, and cryptocurrency. He only considers Bitcoin because it is classified as a “commodity”.

Keeping it real makes sense

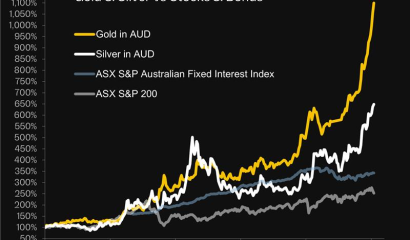

With unreal levels of debt propelling us to the next phase of this crisis, it may make sense to be invested in things that are real.

Thematically that means “assets with limitations on their supply”, in other words things that are scarce. In the case of energy shares, while share floats can expand, the underlying energy resources cannot just be printed at will.

So while the 60/40 share/bond mix served very well growing capital for the past 20+ years, the conditions looking forward could justify a new approach designed primarily to preserve what you’ve got.

And in the case of gold, Rush has you covered.