Many hot takes on what caused the Silicon Valley Bank and Credit Suisse bailouts are now out in the media.

Some have written about the fact that only one of the ten members of the Silicon Valley Bank (SVB) board of directors had any relevant banking experience.

In the case of the shotgun marriage between Credit Suisse and UBS (which required the Swiss government to change the law so that UBS shareholders could not vote on the idea), the focus seems to be on whether bank bondholders were treated fairly.

Most commenters have pointed to the rise in interest rates, which reduced the value of the high-quality government bonds these banks held.

But we would pin the root cause on the central bank zero interest rate policies of the last decade or so.

As noted economist and fund manager Daniel Lacalle points out:

“A decline in value of bonds, mortgages or investments should not bring the collapse of a bank and a contagion risk. What makes banks so fragile? The fact that banks need to leverage those positions multiple times to get a return that, even after increasing debt, is still below cost of capital. And why is the return on assets and equity so poor in banks? Years of repression of interest rates and inflation of sovereign bonds”.

“The reader may say that easy money has helped the economy recover from a severe crisis created by excessive risk-taking, yet it seems that no one remembers that the real estate and tech bubbles of the past were fuelled in the first place by cheap money incentive created by the regulation and the central bank”.

“If rates floated freely, the interest rate on riskier activities would rise faster and prevent accumulation of risk. Furthermore, if central banks did not perpetuate the disguise of risk through purchases of sovereign bonds at any price, the lowest-risk asset would not create a domino effect of valuation and price increases nor the subsequent collapse”.

Is the crisis over?

On the Friday before the crisis the U.S. Federal Reserve said they “had all of the tools necessary to address the situation”. The following Monday they announced a brand-new tool.

This new tool allows banks like SVB to borrow against bonds they hold at imaginary values. A bond with a market value of 60, for example, can be borrowed against at a value of 100.

(Inquiring minds might say: Hey, wait, I have bond losses just like that in my super plan too, do I get a bailout? Or are bailouts just for connected bankers, just like in 2008?).

This bailout is to be paid for by the Federal Deposit Insurance Corporation (FDIC), including the portion of deposits above the insured threshold of $250,000.

But some have noted that the FDIC has just $118 B in capital that is supposed to cover U.S. bank deposits totalling $22 trillion.

So far the market is unimpressed

The SVB bailout was announced by The White House last Monday. The next day, after the announcement, the Eurodollar futures curves went ballistic:

On the left of the chart is the Dot Com crash, in the middle is Lehman/GFC. The market reaction after the bailouts can be seen in the line at the far right.

The Eurodollar futures market is the best barometer of what is happening in the deepest parts of the world’s financial plumbing. This is because two out of three U.S. Dollars trade outside the U.S. (this has come to be known as the “Eurodollar market”).

This chart and the markets are telling us a few things:

1. The market does not believe that the situation has been contained by bailing out 3 U.S. banks that represented less than 2% of the US banking system;

2. The market also does not believe that the Credit Suisse/UBS marriage will stem the problem (default insurance on UBS soared in price after the merger was announced);

3. So the biggest market participants (banks, central banks, investment funds, hedge funds, and insurance companies) are doing everything they can to reduce risk;

4. And they are doing everything they can to get their hands on top-quality collateral.

Do as they do, not as they say

We’ve had indications for a while that there are big systemic problems that have built up over 12 years of money printing and zero interest rates.

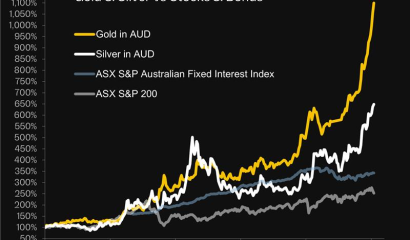

One indicator is the fact that central banks, the ones who are supposed to know the most about banking, have been buying gold at the fastest pace in 40 years.

With the Rush Gold app and just a few clicks you can reduce your risk, especially systemic risk, and get your hands on history’s most reliable store of wealth. You can even use it to tap and pay, just like a bank account, with the Rush Mastercard.

When you own gold with Rush, your wealth is held independent of the banking system. So you can do as the big money is doing, and worry much less about the dramas unfolding by the day in the press.