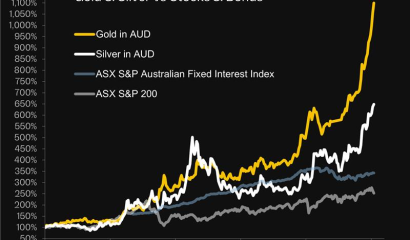

When an investment asset has successfully protected wealth across 4,000 years of human history it is important to understand precisely how it has accomplished this remarkable feat.

Gold bullion has protected wealth across generations because it has protected its owners from what is known as “systemic risk”. Only gold ownership arrangements that provide this systemic risk protection are afforded the full multi-generational benefits of owning gold.

“Systemic risk” refers to the systems used to track and account the ownership of financial wealth. When these systems fail the wealth accounted by them also fails.

Financial system failures are recurring events and can be major or minor. Major failures have occurred during depressions, changes in government, and banking crises. An example of a minor failure was when the bankruptcy proceedings against MF Global resulted in gold fund owners being paid out at $0.70 on the dollar.

More recently, the collapse of Silicon Valley and Signature Bank in the U.S., and the nationalisation of the two remaining megabanks in Switzerland (Credit Suisse and UBS), remind us that money in the bank is simply a promise to you by the bank to pay your funds out when you need them.

In other words, if the one making the promise (the bank) does not stay solvent, then they cannot make good on their promise that your wealth is safe. And while there are government deposit protection schemes in place, these are nowhere near large enough if enough people want to remove their funds from the bank at the same time.

In the U.S. the bank guarantee fund (the FDIC) has just $118 billion in capital that covers more than $22 trillion in bank deposits.

The Gold Standard of Gold Ownership

The gold standard of gold ownership is the outright individual ownership of physical gold metal, full stop. When additional parties are introduced in between the investor and their gold then the gold holding becomes subject to these additional systemic risks.

The providers of financial gold arrangements (like pools, funds, and ETFs for example) are very clear in their product disclosure statements about these additional risks. One such fund (typical of most in the industry) lists the following:

Rather than delivering physical gold to the Fund at the time of purchase, the Gold Vendor will retain legal ownership of the gold in its name.

This means that the Fund does not own gold, the Fund owns a credit obligation of the Gold Vendor, subject to the systemic risk of that vendor. These and other systemic risks are also identified in the PDS:

The Fund may suffer loss if the Gold Vendor, the Gold Dealer, the Gold Custodian, or any other counterparty defaults on its obligations under the relevant contract.

This is further explained:

Legal ownership of the gold remains with the Gold Vendor and the gold is held by the Gold Custodian (in the Gold Custody Accounts) on behalf of the Gold Vendor and not on behalf of the Fund. The rights and economic exposure of the Fund in relation to gold arise pursuant to the Gold Contract and not through a physical holding of gold.

Knowing your Rights as a Gold Investor

Given the role that gold plays in the long-term preservation of capital, reading the terms of a gold investment should be done as carefully as reading the coverages and exclusions in an insurance policy.

With a gold investment you are insuring your wealth against a set of financial risks, just as you might insure your home, your business, or your loved ones against a catastrophic loss.

All Rush Gold customers are the individual outright owners of physical gold bullion, full stop. All customers are issued with a timestamped receipt detailing the gold in weight and purity they have purchased as proof of ownership. There is no intermediary standing between customers and their direct ownership of gold: the customers own their gold outright and only they can direct what happens to it.

This simple structure means that Rush Gold customer gold is protected under property rights laws, the same laws that protect the ownership of other real property like houses and fine art. These property rights are enshrined in the Constitution of Australia and are rated as the sixth strongest of the 195 countries in the world (according to the International Property Rights Alliance). It is absolutely against the law for a federal, state, local government, or any other party, to infringe the property rights of an individual without due process. Those rights are not affected by banking crises.

Real Gold can also have lower long-term Ownership Costs

In addition to the wealth insurance benefits of physical gold, it also tends to be less expensive to own over the long term. Gold derivatives like ETFs tend to have lower initial costs but have higher ongoing fee structures to compensate the various intermediary providers like trustees and sub-custodians. Higher ongoing costs would reduce overall returns.

So funds like ETFs provide investors with exposure to changes in the price of gold but do not provide investors with the systemic risk protections that are the key feature that has made gold a successful store of wealth regardless of what transpires in the world around it.

Gold is gold and funds are funds. When seeking the true wealth protection of an asset that has stood the test of time more and more investors are making sure they own the real thing.